Opportunity Zones

May 3, 2018

Opportunity Zones are a new community development program established by Congress in the Tax Cuts and Jobs Act of 2017 to encourage long-term investments in low-income urban and rural communities nationwide. The Opportunity Zones program provides a tax incentive for investors to re-invest their unrealized capital gains into Opportunity Funds that are dedicated to investing into Opportunity Zones designated by the chief executives of every U.S. state and territory. This program uses low-income community census tracts as the basis for determining areas eligible for Opportunity Zone designation. The Opportunity Zones program offers investors the following incentives for putting their capital to work in low-income communities:

• A temporary tax deferral for capital gains reinvested in an Opportunity Fund. The deferred gain must be recognized on the earlier of the date on which the opportunity zone investment is sold or Dec. 31, 2026.

• A step-up in basis for capital gains reinvested in an Opportunity Fund. The basis of the original investment is increased by 10 percent if the investment in the qualified opportunity zone fund is held by the taxpayer for at least five years, and by an additional five percent if held for at least seven years, excluding up to 15 percent of the original gain from taxation.

• A permanent exclusion from taxable income of capital gains from the sale or exchange of an investment in a qualified opportunity zone fund, if the investment is held for at least 10 years. (Note: this exclusion applies to the gains accrued from an investment in an Opportunity Fund, not the original gains). The recent Tax Cuts and Jobs Act has provided favorable tax treatment with respect to the timely reinvestment of realized capital gains into Qualified Opportunity Funds.

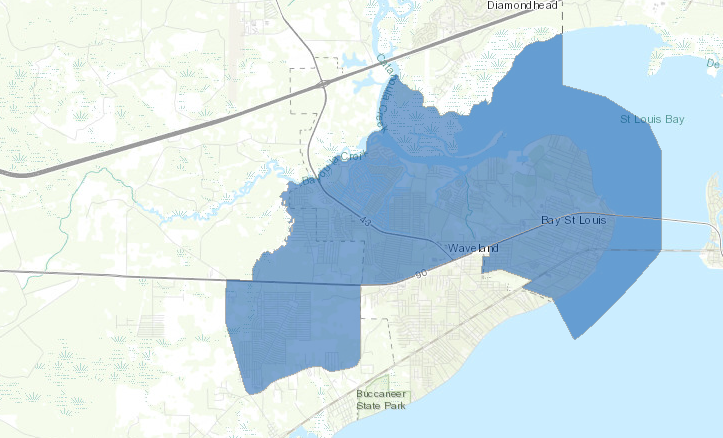

Are there any Qualified Opportunity Zones in Hancock County?

Hancock County’s Opportunity Zones cover portions of Bay St. Louis and Waveland and are census tracts 28045030100 and 28045030300. A map can be found here: https://www.mississippi.org/opportunity-zone-map/

What are the tax advantages of holding an investment for designated time periods?

Realized capital gains that are reinvested into a Qualified Opportunity Fund within 180 days are not taxed until the investment in the fund is sold, or Dec. 31, 2026, if earlier (the “recognition date”). If the fund investment is held for 5 years prior to the recognition date, the taxpayer’s basis is stepped up such that 10 percent of the invested deferred gain escapes taxation. If the fund investment is held seven years, an additional five percent of the deferred gain escapes taxation. (Deferred gains invested within five years of Dec. 31, 2026 will be taxed in full in the 2026 tax year regardless of how long they are held after that, but the taxpayer’s basis in the fund investment may still be eligible for a step-up in basis at the five and seven year marks.) If the fund investment is held for 10 years, capital gains taxes will be due for 2026 with respect to the deferred gain rolled over into the fund (taking into account the basis adjustments described above), but the taxpayer in the year of sale can elect to adjust his basis to the then fair market value such that “new” gain on the fund investment will not be taxed.

What is a “Qualified Opportunity Fund”?

A Qualified Opportunity Fund is a corporation or partnership organized for the purpose of investing in “qualified opportunity zone property” and that holds 90 percent of its assets in “qualified opportunity zone property.” The Act directs the Department of Treasury to prescribe rules for the certification of Qualified Opportunity Funds. The certification process is expected to be handled by the Community Development Financial Institutions (CDFI) Fund in a similar manner to the existing process for allocating New Markets Tax Credits.

What are the investment requirements applicable to Qualified Opportunity Funds?

A Qualified Opportunity Fund must hold at least 90 percent of its assets in “qualified opportunity zone property,” determined by the average of the percentage of such property held by the fund on the last day of the sixth month and on the last day of each tax year. If the Qualified Opportunity Fund fails to meet the 90 percent test, it (or its owners if it’s a pass-through entity) will pay a tax penalty on a sliding scale.

What sorts of investments constitute “qualified opportunity zone property”?

A Qualified Opportunity Fund can invest directly in tangible property used in a trade or business if (i) such property was acquired by purchase after Dec. 31, 2017, (ii) the original use of such property commences with the Qualified Opportunity Fund or the Qualified Opportunity Fund substantially improves the property, and (iii) substantially all of the use of such property is in a qualified opportunity zone. It can also invest cash in newly issued securities of certain corporations or partnerships substantially all of whose tangible property meets the tests of clauses (i), (ii) and (iii) above. Projects that could qualify are construction or substantial rehabilitation of commercial properties or single or multi-family residential properties and operating businesses. (Certain disfavored businesses are excluded, such as golf courses and gambling establishments.)

Must the fund’s investments be physically located in a qualified opportunity zone?

To qualify as “qualified opportunity zone business property,” substantially all of the use of such property must be in a qualified opportunity zone. Unless and until further guidance is issued, it is recommended to interpret this requirement as requiring physical presence.

What applicable Treasury guidance is available?

Revenue Procedure 2018-16 provides guidance relating to the eligibility of certain census tracts for nomination and approval as “qualified opportunity zones.” No other Treasury guidance is yet available.

Are capital gains realized in 2017 eligible?

The Act has an effective date of Dec. 22, 2017. Certainly, capital gains realized in a transaction with an “unrelated person” on or after that date are eligible if timely reinvested into a Qualified Opportunity Fund. It is not certain whether capital gains realized before the effective date are eligible. [As a practical matter, unless certified Qualified Opportunity Funds are accepting investments before mid-June, 2018, a taxpayer could not take advantage of the new law for 2017 gains.]

What will be the effect of timely reinvestment of eligible 2017 capital gains with respect to the 2017 tax year?

Taxpayers who timely reinvest eligible 2017 capital gains into a Qualified Opportunity Fund and make the required tax election will not be taxed on those capital gains in the 2017 tax year. They will incur tax liability on those gains in the year they sell their investment or 2026, if earlier, at the applicable capital gains rates then in effect, subject to potential favorable basis adjustments.

Are capital gains realized in 2018 eligible?

Capital gains realized in a transaction with an “unrelated person” in 2018 and thereafter through Dec. 31, 2026 are eligible.

What are the reinvestment requirements for favorable capital gains tax treatment?

In order to qualify for the Act’s favorable capital gains tax treatment, eligible capital gains realized in a sale or exchange must be reinvested in a Qualified Opportunity Fund within 180 days.

What if investments are made in a zone prior to its designation as a qualified opportunity zone? Will it qualify if the zone is subsequently approved for designation?

All opportunity zones should be designated no later than June 20, 2018. Therefore, it is recommended that qualified opportunity funds wait to make investments until that time. (But a taxpayer could make his investment in a qualified opportunity fund prior to the zone designations.)

The information contained herein is a summary and general in nature. It is not, and should not be construed as, accounting, legal or tax advice and may not be applicable to, or suitable for, the reader’s specific circumstances or needs which may require consideration of tax and nontax factors not described herein. The reader should contact his own tax advisor prior to taking any action based upon this information. Changes in tax laws or other factors could affect, on a prospective or retroactive basis, the information contained herein.